Factor Investing vs Smart Beta: Complete Guide to Key Differences and Applications

- What Is Factor Investing?

- How Factor Investing Works

- Common Investment Factors

- Value Factor

- Quality Factor

- Momentum Factor

- Size Factor

- Low Volatility Factor

- Dividend Yield Factor

- What Is Smart Beta?

- Key Characteristics of Smart Beta:

- Factor Investing vs. Smart Beta: Key Differences

- Strengths of Factor Investing and Smart Beta

- Evidence-Based Approach

- Reduced Behavioral Bias

- Potential Outperformance

- Lower Costs

- Diversification Along Factor Dimensions

- Transparency and Control

- Weaknesses and Limitations

- Cyclic Underperformance

- Crowding Risk

- Complexity

- Factor Rotation Challenges

- Front-Running and Rebalancing Costs

- Data-Mining and Over-Fitting

- Behavioral Hurdles

- Practical Applications of Factor Investing

- Application 1: Building a Core Portfolio

- Application 2: Complementing Active Management

- Application 3: Tactical Factor Allocation

- Application 4: Fixed Income and Beyond

- Application 5: International and Emerging Markets

- How to Get Started with Factor Investing

- Step 1: Assess Your Time Horizon and Risk Tolerance

- Step 2: Choose Your Factor Exposure

- Step 3: Select Implementation Vehicle

- Step 4: Commit to a Rebalancing Schedule

- Step 5: Monitor and Adjust Sparingly

- Common Factor-Based Products

- Conclusion

In the era of low-cost index funds and algorithmic trading, a new investment paradigm has emerged that sits somewhere between passive index investing and active stock picking. This middle ground is known as factor investing, often implemented through smart beta strategies. Both terms are frequently used interchangeably, yet they represent distinct concepts that can significantly impact your investment returns and portfolio risk.

If you've ever wondered why certain stocks consistently outperform the market while others underperform, or why some investment strategies work better than others, factor investing provides a data-driven answer. This article breaks down these concepts, explains how they differ, and shows you how to apply them in practice.

What Is Factor Investing?

Factor investing is an investment strategy that selects securities based on measurable characteristics—known as factors—that have been historically associated with higher returns or lower risk. Rather than trying to pick individual winning stocks or timing the market, factor investing relies on decades of academic research showing that certain traits consistently drive returns across different market conditions.

The concept originated with Stephen A. Ross's arbitrage pricing theory in 1976, which challenged the prevailing Capital Asset Pricing Model (CAPM). CAPM suggested that a stock's returns were determined primarily by its market beta—its sensitivity to overall market movements. However, empirical research revealed that this model was too simplistic. Sanjoy Basu documented a value premium in 1977, showing that undervalued stocks outperformed expensive ones. Shortly after, Rolf Banz discovered the size premium, proving that smaller companies outperformed larger ones over long periods.

These discoveries fundamentally changed how professional investors approached portfolio construction. If specific characteristics could predict returns, why not systematically tilt portfolios toward these characteristics?

How Factor Investing Works

Factor investing operates through a straightforward process:

Identify factors with historical evidence of outperformance (value, momentum, quality, size, low volatility)

Score and rank securities based on how well they exhibit these factors

Overweight securities with strong factor characteristics

Underweight or exclude securities with weak factor characteristics

Rebalance periodically to maintain factor exposure

This systematic, rules-based approach removes emotion from investing. You're not betting on individual companies; you're gaining exposure to proven return drivers.

Common Investment Factors

Value Factor

Value stocks trade at low prices relative to their fundamentals—earnings, cash flow, or book value. Investors often favor them because they appear "cheap", and historically, value has been one of the most robust factors. A common metric is the price-to-earnings (P/E) ratio: lower P/E stocks are considered more valuable. Academic research suggests value outperforms over long periods, though it can underperform significantly during growth-driven bull markets.

Quality Factor

Quality companies exhibit high and stable profitability, strong balance sheets, low debt levels, and consistent earnings across business cycles. Interestingly, high-quality companies often outperform while taking on less risk—a paradox that challenges traditional financial theory. Quality metrics include return on equity (ROE), return on assets (ROA), debt-to-assets ratios, and earnings stability. During market downturns, quality stocks typically decline less than lower-quality competitors.

Momentum Factor

Momentum captures the tendency of stocks that have performed well recently to continue performing well in the near term. A momentum strategy ranks stocks by their 6-12 month returns and overweights top performers. While momentum can deliver strong returns, it also tends to "crash" unexpectedly, making it one of the more volatile factors. Momentum works particularly well in strong trending markets.

Size Factor

The size factor targets market capitalization. Small-cap stocks have historically outperformed large-cap stocks over very long periods, though with higher volatility. This premium has been more pronounced in certain decades and less evident in others. Small-cap value strategies combine both factors, targeting undervalued smaller companies.

Low Volatility Factor

Low volatility strategies select stocks with historically lower price swings (measured by standard deviation or beta). Counterintuitively, these stocks often deliver superior risk-adjusted returns while experiencing fewer price fluctuations. During market crashes, low-volatility stocks tend to hold up better than the broader market.

Dividend Yield Factor

This strategy focuses on stocks paying higher-than-average dividends. Dividend-paying stocks typically have more stable businesses and are often viewed as less risky. However, this factor can underperform during growth-driven markets.

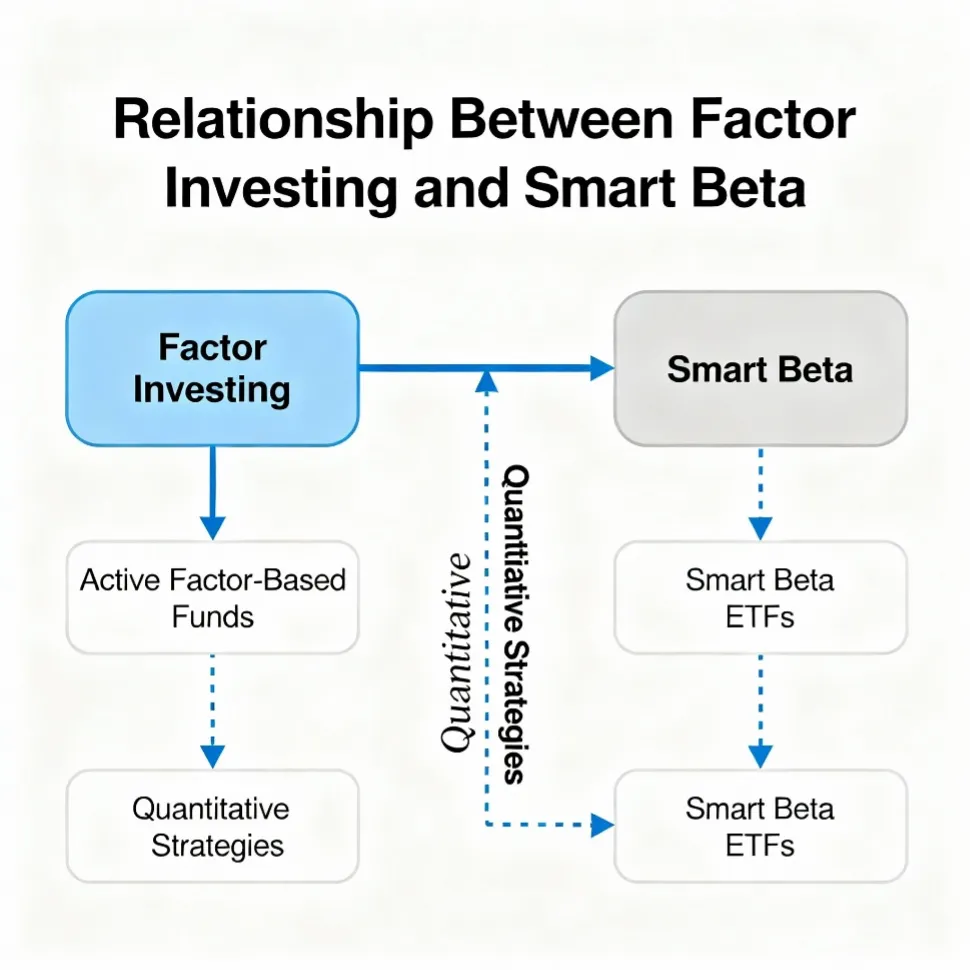

What Is Smart Beta?

Smart beta is a specific implementation method for factor investing. While factor investing is the broader concept of targeting specific return drivers, smart beta is the practical application—often through ETFs—that aims to capture these factors systematically and cost-effectively.

The term "smart beta" reflects its position between traditional index investing and active management. A regular beta index (like the S&P 500) weights companies by market capitalization—meaning the largest, most expensive companies get the most influence. Smart beta uses alternative weighting schemes based on factors, seeking to capture the "smart" part: the factors that drive returns.

Key Characteristics of Smart Beta:

- Rules-based approach – All decisions follow predetermined rules, eliminating manager discretion and emotional biases

- Transparent – Unlike active managers, you know exactly which stocks are included and why

- Lower costs – Smart beta ETFs typically charge 0.20% to 0.50% annually, compared to 1% or more for active funds

- Systematic rebalancing – Portfolios rebalance on a fixed schedule, maintaining consistent factor exposure

- Flexible weighting – Can use equal-weighting, fundamental weighting, or other alternatives to market-cap weighting

Factor Investing vs. Smart Beta: Key Differences

| Aspect | Factor Investing | Smart Beta |

|---|---|---|

| Scope | Broader concept—any strategy targeting specific return factors | Specific implementation, usually through passive rules-based products |

| Implementation | Can be active, passive, or hybrid | Primarily passive or semi-passive |

| Flexibility | Highly flexible—can use any factors and methods | Rules-based, predetermined methodology |

| Product Form | Mutual funds, ETFs, direct stock portfolios, options, futures | Mainly ETFs and indexes |

| Active Management | May involve active decisions | Purely rules-based, no active manager discretion |

| Transparency | Varies; active managers may have discretion | Highly transparent—methodology published |

| Cost | Ranges from 0.20% (passive) to 1%+ (active) | Typically 0.20% to 0.50% annually |

| Customization | Highly customizable to specific investor needs | Limited to predefined factor exposures |

| Historical Context | Rooted in 1970s academic research | Emerged as commercialized application in 2000s |

Think of it this way: all smart beta is factor investing, but not all factor investing is smart beta. An investment manager might actively use factor research to pick individual stocks—that's factor investing. An ETF tracking a value-weighted index constructed around the quality factor—that's smart beta.

Strengths of Factor Investing and Smart Beta

Evidence-Based Approach

Unlike stock-picking based on hunches, factor investing rests on decades of academic research and historical data. Factors like value and momentum have documented outperformance across multiple decades and markets, providing confidence in the strategy.

Reduced Behavioral Bias

By following systematic rules, factor investing removes the emotional decision-making that often hurts investor returns. You're not tempted to "chase" hot stocks or panic-sell during downturns.

Potential Outperformance

Historically, many factors have delivered returns exceeding broad market indices. A well-constructed multi-factor portfolio can capture persistent return premiums while reducing portfolio risk.

Lower Costs

Smart beta ETFs charge significantly less than actively managed funds. With expense ratios typically between 0.20% and 0.50%, you keep more of your returns instead of paying for active management.

Diversification Along Factor Dimensions

By combining multiple factors (value + quality + momentum), you reduce reliance on any single factor and smooth returns across different market regimes.

Transparency and Control

Smart beta strategies are completely transparent—you know the rules before investing. This contrasts with active managers who may change their approach without notice.

Weaknesses and Limitations

Cyclic Underperformance

No single factor outperforms consistently. Value can lag for years during growth-driven markets (as it did from 2015-2020), while momentum can crash suddenly. This requires patience and discipline from investors.

Crowding Risk

As more capital flows into factor-based strategies, some worry that factor premiums will erode through crowding. If everyone exploits the same factors simultaneously, those opportunities may disappear.

Complexity

Combining multiple factors can be tricky. Overlapping signals can dilute each factor's advantage if not carefully constructed. Different providers may define "value" or "quality" differently, leading to performance divergence.

Factor Rotation Challenges

Knowing which factors will work best in different market environments is difficult. Multi-factor strategies may contain conflicting signals—value and momentum sometimes work in opposite directions.

Front-Running and Rebalancing Costs

Large-scale factor rebalancing can move markets, potentially hurting performance. Smaller factor ETFs may have slippage costs that reduce returns.

Data-Mining and Over-Fitting

Some factors may reflect statistical anomalies rather than fundamental economic drivers. Academic research sometimes uncovers factors that simply won't persist in real-world trading.

Behavioral Hurdles

Investors often abandon factor strategies right after underperformance. A value investor who panics and exits after years of underperformance misses the subsequent recovery, locking in losses.

Practical Applications of Factor Investing

Application 1: Building a Core Portfolio

An investor seeking long-term growth with lower risk might combine multiple factors: 50% value, 30% quality, and 20% momentum across diversified sectors. This multi-factor approach provides:

Stability through quality and value (defensive)

Growth potential through momentum

Lower volatility than aggressive growth portfolios

Lower costs than active management

Application 2: Complementing Active Management

Some investors use factor investing as a complement to active strategies. A base portfolio of factor-based ETFs (70-80%) provides consistent, lower-cost returns while a smaller allocation to active managers (20-30%) pursues higher returns. This "barbell" approach balances costs and potential outperformance.

Application 3: Tactical Factor Allocation

Sophisticated investors tactically allocate between factors based on market conditions. During periods of economic uncertainty, they might increase quality exposure. During strong economic growth, they might emphasize momentum or small-cap factors. This requires active monitoring but can improve returns.

Application 4: Fixed Income and Beyond

Factor investing extends beyond equities. Fixed-income factor strategies (quality bonds, value bonds), commodity factor strategies, and multi-asset factor approaches exist. An investor might build a diversified portfolio combining equity factors, bond factors, and real assets.

Application 5: International and Emerging Markets

Factor exposure extends globally. Many investors apply the same factor discipline to emerging markets, finding that value, quality, and momentum factors work in different geographies, providing diversification benefits.

How to Get Started with Factor Investing

Step 1: Assess Your Time Horizon and Risk Tolerance

Factor investing works best for long-term investors (5+ years) who can tolerate drawdowns. If you need money within 2-3 years or become anxious during market declines, a simpler strategy may suit you better.

Step 2: Choose Your Factor Exposure

Decide which factors align with your goals:

- Conservative investors: quality + low volatility

- Growth-oriented investors: momentum + value

- Balanced approach: multi-factor combination (quality, value, dividend yield)

Step 3: Select Implementation Vehicle

Choose how to implement your strategy:

- ETFs: Most accessible for individual investors (lowest costs)

- Mutual Funds: More variety, slightly higher costs

- Robo-Advisors: Automated factor-based portfolios (moderate costs)

- Direct Management: For sophisticated investors with large portfolios

Step 4: Commit to a Rebalancing Schedule

Establish a rebalancing frequency (quarterly, semi-annually, annually) and stick to it. This maintains factor exposure and prevents "winners" from dominating your portfolio.

Step 5: Monitor and Adjust Sparingly

Track your portfolio's factor exposures and performance relative to benchmarks. Make changes only if your investment thesis changes, not based on short-term performance.

Common Factor-Based Products

Several major ETF providers offer factor-based products:

- iShares Factor ETFs: Comprehensive suite covering value, quality, momentum, low volatility, dividend factors

- Vanguard Factor ETFs: Similar offerings from one of the largest asset managers

- SPDR Factor ETFs: Alternative factor definitions and geographic exposures

- Schwab Factor ETFs: Lower-cost options for discount brokerage clients

These products typically have expense ratios of 0.20%-0.50%, compared to 1%+ for actively managed funds.

Conclusion

Factor investing and smart beta represent a significant evolution in how individual and institutional investors can build portfolios. By shifting from emotion-driven stock picking to evidence-based factor targeting, investors gain access to proven return drivers at lower costs than traditional active management.

The key difference lies in scope: factor investing is the broad strategy of targeting specific return drivers, while smart beta is a specific, rules-based implementation usually through ETFs. Both offer compelling advantages—systematic discipline, transparency, lower costs, and potential outperformance—but neither is a guaranteed ticket to riches. Factors cycle in and out of favor, performance can underperform for years, and crowding can erode premiums.

For most investors, a long-term multi-factor portfolio implemented through low-cost smart beta ETFs offers an attractive middle ground between passive index investing and expensive active management. Whether you're a beginner building your first portfolio or an experienced investor seeking to refine your approach, understanding factors and smart beta provides powerful tools for constructing a more intentional, evidence-based investment strategy.